BANKEX, founded in 2015 by Igor Khmel, Ilham Hatypov, and Dmitry Dolgov, aims to meet the demand of improving asset liquidity using a proprietary Proof of Asset protocol designed to enable information to be passed in real time directly to and from the blockchain.

[Note: This is a sponsored article.]

This technology is transferring the information about an asset to the blockchain enabling fast transactions and avoiding cumbersome rules and regulations of a traditional stock exchange.

By taking advantage of technologies like the Internet of Things (IoT) and Artificial Intelligence (AI) in order to create Internet of Assets (IoA) BANKEX is building a new standard of decentralized financial market.

The PoA protocol can be used by various entities from Fintech providers, including AI and IoT labs, and traditional financial institutions to any asset owner. BANKEX, based on Bank-as-a-Service (BaaS), is evolving ordinary transaction mechanisms. All the transactions that are carried out using PoA are faster, clearer and much more reliable. This technology ensures that every single token is backed by a real asset. The PoA increases the liquidity of real-world assets while delivering constant real-time updates to both asset owners and investors.

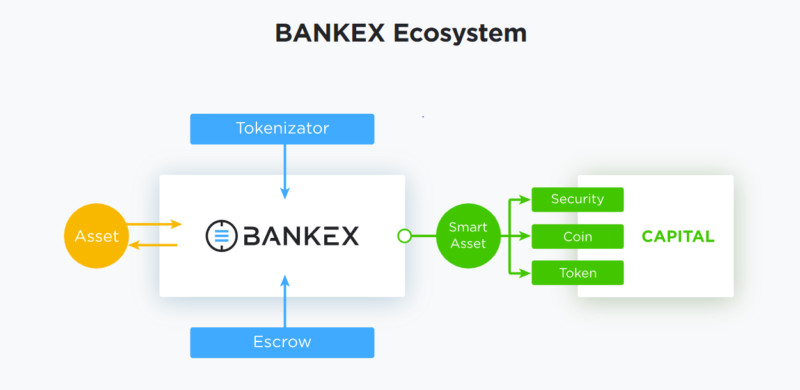

Asset Tokenization

Tokenization is a process that transforms data on an asset into an encrypted code, also known as a token, in order to represent this information on the blockchain. BANKEX ensures that all the information about an asset is relevant and correct by delivering verification processes.

Traditional financial markets encounter several problems that lead to lower liquidity of assets, something that BANKEX is looking to fix. Such issues include but are not limited to:

- Large numbers of asset owners result in poor communication.

- High dispersion of an asset makes it difficult to control detailed cash flow from each asset

- Start projects and achieve desirable liquidity is very time-consuming

- Inability to enter financial markets and attract sufficient investments for non-public companies.

- Complicated processes of tracking an asset’s lifecycle.

- High legal and accounting expenditures caused by asset transfers when early investors sell their assets at peak profitability.

- Complex procedures of asset retraction in case the terms of the contract are not fulfilled.

How It Works

Bank-as-a-Service (BaaS) works by offering Fintech services without the need of a traditional, bricks and mortar bank. Roles within the BANKEX ecosystem:

- Originator – the owner or owners of an asset

- Supplier – the purchaser of a tokenized asset, i.e. investor.

- Product Owner – the company that creates Fintech products aimed at providing the tech for tokenization, the role, in this case, is carried out by BANKEX.

The process creates a win-win for all involved. Originators receive new opportunities, suppliers can increase their investment portfolio, and product owners benefit from delivering services to originators and suppliers.

BANKEX’s process encompasses 4 stages – Digitisation, Tokenisation, Asset Trading, and finally Dealing.

Digitisation: BANKEX collects and verifies all information regarding a specific asset. – All legal and accounting disputes and issues resolved during this stage.

Tokenisation: smart contracts are created on the Ethereum blockchain. As a result, an asset transforms into a Smart Asset. At this stage, the token is created. If needed BANKEX provides escrow services. The token then goes to market. Tokenization by its nature is the next generation of securitization.

Asset Trading commences, the price is adjusted based on market offers.

Dealing: by using the Proof-of-Mining protocol the token is guaranteed to be delivered to the supplier (investor). The token is delivered to the supplier (investor) and is kept in his wallet, the BANKEX token is delivered to the originator (asset owner).

BANKEX Use Cases

BANKEX PoA can have various applications. Here are a few of them:

Real Estate. An international bank (the client) has a piece of commercial or residential property (the asset) upon which it plans to develop apartments. In this case, the token represents a fixed number of square meters of those apartments (e.g. 1 token = 10 square meters). Investors receive a liquid asset after the to-be-built real estate is tokenized.

Drinking Water for Africa (non-profit). In this scenario, the client is a water filter producer and the asset is frozen drinking water. Charity donors can buy water tokens, with 1 token representing 1 liter of drinking water. After water tokens are purchased, the donor can potentially then track the journey of that water all the way to the end consumer.

Retail Franchise Network. A retail chain (the client) can use their store’s cash flow as an asset. The tokens are backed by revenue generated by royalties from franchises. Tokens can be used to purchase products in the chain stores, with 1 product equal to 1 token. Token owners can buy products from the retail chain, as well as take part in the company’s decision-making process. The business case, in this example, would be to finance expansion and open a new store.

BANKEX has gained support from 10 banks, top tech companies including Microsoft. They are also ranked in the Top 9 ICO by Entrepreneur and is considered to be in the Top 50 Fintech start-ups in the world. During their opening presale, BANKEX raised $10 million, with a further $1.5 million raised prior to the pre-ICO stage.

For additional information about BANKEX, please visit the company website. You can also talk to the BANKEX team on Telegram and follow them on Facebook.

What do you think about BANKEX’s Proof-of-Asset protocol? Will it make the tokenization of traditionally illiquid assets easier and more accessible? Let us know in the comments below.

Images courtesy of BANKEX

The post Proof-of-Asset Protocol by BANKEX – a New Era in the History of Banking Services appeared first on Bitcoinist.com.